Where are the Drones?

There continues to be a lot of discussion in the property and casualty industry about the use of drones as part of the property inspection process. The FAA has even relaxed the use of drones for commercial usage, so where are they and how are they being utilized?

There continues to be a lot of discussion in the property and casualty industry about the use of drones as part of the property inspection process. The FAA has even relaxed the use of drones for commercial usage, so where are they and how are they being utilized?

On June 21, 2016 the FAA announced Part 107 that provided new restrictions and requirements for the commercial usage of unmanned aircraft. These rules, which went into effect on August 29, are broken down into three categories: Operational Limitations, Remote Pilot in Command Certification and Aircraft Requirements.

The Operational Limitations require that the aircraft weight must be less than 55 pounds, the operator must maintain a visual line of sight with the craft and may not operate the craft over any persons not directly participating in the operation unless they are covered by a shelter. Operation is limited to daylight hours only, with maximum altitude of 400 ft. above ground level, and weather visibility of no less than 3 miles. As with any aircraft, the operator is required to perform a pre-flight inspection, and operations within FAA controlled airspace (near airports) are only allowed with the required permission of local Air Traffic Control.

The Remote Pilot in Command requirements are that the operator of these crafts must first successfully complete an on-line test and vetting by the TSA in order to obtain the mandatory piloting certificate. Upon receiving their certificate, operators are required to file reports with the FAA in the event they are involved in any serious injuries or create damage over $500 while operating their aircraft.

Unlike manned aircraft, unmanned aircrafts do not require an airworthiness certificate.

So, do these new regulations create an environment where drones can become a ubiquitous tool of the personal lines insurance surveyor? Well, no, not quite yet. At this time, most commercial uses of drones for property insurance purposes is for survey damage within catastrophe areas, or for large commercial structures. Why the limited use? Well, there are several reasons. Even with the relaxed rules, drone usage for home and most commercial property inspections is still not a practical or an economical approach to inspections. The pilot certification requirements, combined with the cost for equipment and maintenance of the aircraft make the cost of utilizing drones on home inspections excessive; the average drone inspection cost is about $150 per hour. Another big issue is privacy. Currently there are no Federal laws concerning privacy with the use of drones, other than the FAA restriction on using them over uncovered non-participants. Discrete regulation of drone usage within public areas has been left up to states and municipalities, and many states are imposing increasingly restrictive privacy laws with serious consequences. There is also the potential for property damage. A gust of wind or pilot error could cause an aircraft to come into contact with a structure, creating a liability issues for the pilot. All of these issues will continue to hinder the effective use of drones in the surveying of homes for insurance underwriting purposes. Drones will, however, likely play an expanding role in surveying commercial structures, so long as the operation can be performed safely, within the line of sight of the operator, and can ensure against flying over anyone not participating in the operation.

At Millennium, we own several drones with which we conduct periodic experiments in order to assess their potential for enhancing property surveys. Thus far, due to the limitations of the new FAA rules and those of evolving municipal regulations, and the anticipated discomfort of homeowners, we believe a true commercial application for home inspections is still a ways off in the future. For these same reasons, a broad application for commercial inspections is also limited at this time. Nonetheless, we will continue to monitor the regulatory environment surrounding drone usage, and seek out the right solution for utilizing drones in conducting surveys in ways which are both economical and beneficial to our clients.

For many years, the Insurance industry has been mining data to better understand how their new business should perform and to get an actionable view into their existing Book of Business. At Millennium Information Services, we also believe in the power of data by giving our clients insight into their inspection data through our comprehensive, detail-rich property survey reports, state-of-the-art data mining and analytical tools, and valuable inspection metrics that categorize and assess property risks that can all be used to make intelligent, insightful underwriting decisions.

It begins with intelligent data. All data tells a story and specifically, property data, can give a carrier a view into the quality of new business submissions, and also provide the underwriter better insight into the condition and hazards of a property to make intelligent decisions that best follow the underwriting guidelines of their company. Millennium captures hundreds of property and risk characteristics, including home construction features, policy rating variables, and conditions, hazards, and liability exposures. This detailed property data is fed into Millennium’s Automated Property System (“MAPS”), which serves not only as a data warehouse and workflow management tool, but offers a robust, flexible set of reporting capabilities which allow carriers to easily mine and analyze their inspection data. Identified issues are referred and assigned a weighted score (“Referral Value”) based on severity and the level of the underwriting concern. The sum of these weighted scores represents the Total Referral Value for each inspection – a discreet, policy-level indication of the cumulative severity of all noted conditions. Each inspection is also assigned a unique indicator, or Stack Logic® code, based on the prioritized outcome of the inspection (e.g., types of conditions observed, occupancy status, insurance-to-value opportunity, etc.). These qualifiers transform raw inspection information into Intelligent Data from which precise underwriting decisions can be made objectively.

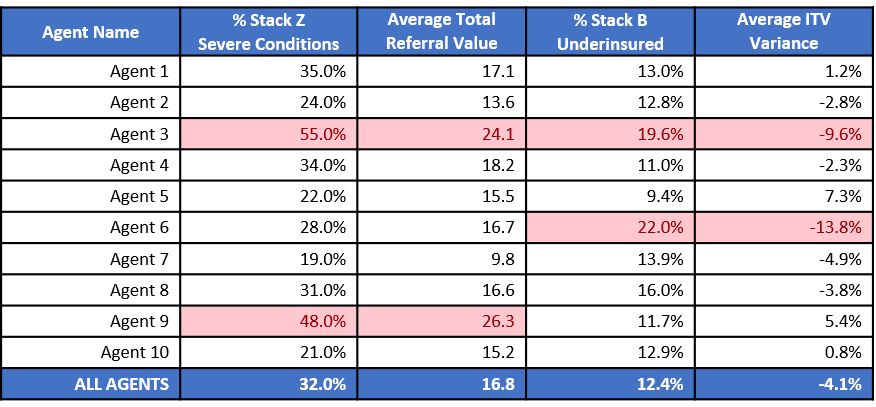

Evaluating agency performance is one opportunity that is provided through utilizing Intelligent Data. The chart below shows how, with the use of MAPS Ad Hoc reporting capabilities, a quick analysis of Stack Logic and Referral Values by Agent can be used to easily identify agents with a quality of business and/or excessive ITV deficiencies on policies submitted. Using pre-qualified, Intelligent Data allows policy quality analysis to be constructed quickly and for trends to be easily identified and monitored, long before profitability is impacted.

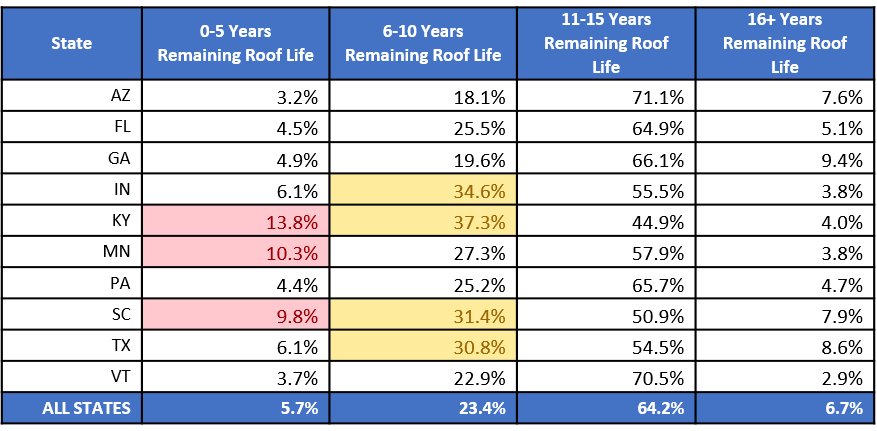

Identifying, understanding and being able to quickly respond to regional trends in conditions and hazards is also promoted through the evaluation of Intelligent Data. Roof damage is one of the most significant source of claim activity across the property and casualty insurance industry. That’s why, in addition to Stack Logic and Referral Values, we’ve developed our Roof Life Indicator. On each inspection report, along with comprehensive, detailed photo documentation, we provide assessment of the remaining roof life, broken into 4 categories, based on the observed condition of the roof at the time of inspection: 0 to 5 years, 6 to 10 years, 11-15 years, and 16+ years. Like Stack Logic and Referral Values, the Roof Life Indicator can be used not only to develop consistent action guidelines for individual risks – from roof repair/replacement to ACV roof endorsement to future re-inspection – but also to analyze the inspection book and easily identify those segments where roof age and condition issues are more prevalent. For example, take a look at the chart below showing the distribution of Roof Life Indicator by state:

With MAPS’ dynamic reporting capabilities, carriers can easily drill down below the state level and view roof life indicator results at a county, city or zip code level to identify specific geographic areas where increased underwriting focus and action may be needed to mitigate future roof losses.

These are just a few examples of how Millennium is helping carriers to manage and improve the quality and profitability of their business through the use of data and data analytics. Intelligent Data, smarter decisions – that’s the Millennium advantage.

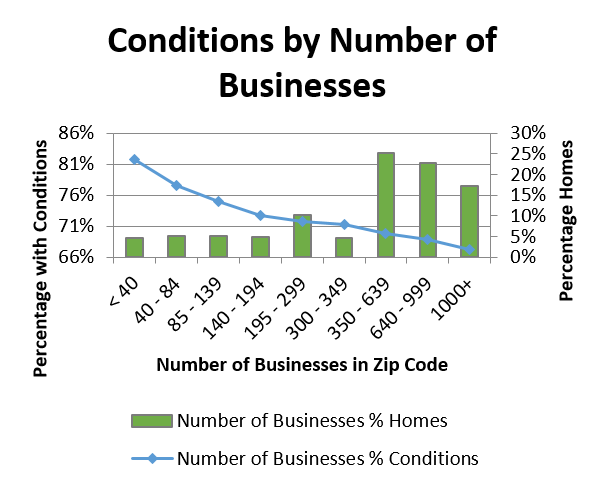

Did you know that the concentration of businesses in an area is predictive of potential underwriting concerns in surrounding homes?

We didn’t, until we embarked on the development of our inspection optimization model, PreInspectR®. We analyzed that factor, in addition to 50 other policy, home, environmental and geographic variables, for inclusion in our model scores.

We were surprised to discover that many attributes long relied upon by carriers were not the most effective at selecting risks for more intensive underwriting evaluations. Additionally, some others, like concentration of businesses (see chart below), made more effective contributions to scoring accuracy when combined with other, more predictive attributes.

All carriers need to examine their property books on a regular basis, but few have the budget to inspect all of it every year. Relying on traditional attributes like age and total living area is inadequate. Some data and modeling companies have developed expensive solutions that provide scores based on non-property related elements, such as consumer credit. At Millennium, we took a different approach. Our inspection optimization model, PreInspectR, is built entirely on property and geographically relevant data points.

Our model is built with 25 years of inspection knowledge and the use of our robust 12-million-record-inspection database, along with other geospatial and environmental data.

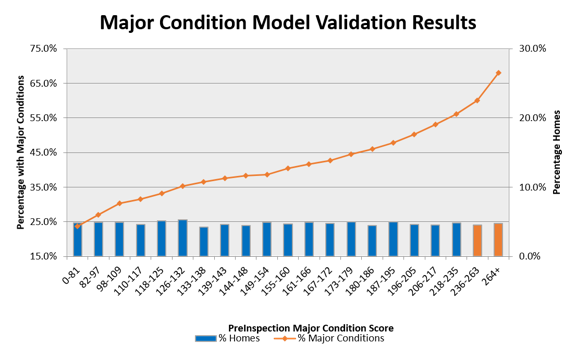

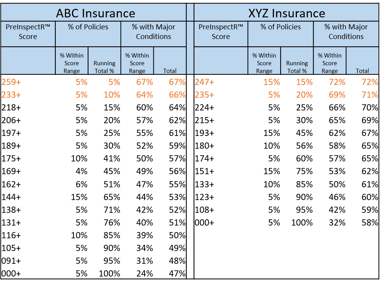

We found that the combination of these data variables in our PreInspectR model were very predictive of underwriting concerns. You can see that in the accompanying chart below, which illustrates the frequency of major underwriting concerns within score segments, each representing 5% of the population of inspections. Note, that looking at the worst scoring 10% of the book would result in an actionable rate of over 65%!

In the two real-life examples below, you will see that these companies could look at 10% and 20% of their book and have an actionable rate on Major Conditions of at least 66% and 71% respectively, based upon the PreInspectR scoring algorithm.

From an economic perspective, PreInspectR helps identify those properties that have the highest probability of having issues that need either remediation or cancellation, ensuring the avoidance of a claim in the future. It also assists in the identification of properties that have ITV issues where a coverage and premium increase is necessary to generate a healthy ROI.

The process for scoring a book using PreInspectR is simple. All that is required is five specific property characteristics from each policy. The scores produced for each property will indicate the likelihood of condition hazards and/or ITV concerns. This allows you to focus on those properties with the highest scores, which in turn will have the highest actionable rate. Using this approach, PreInspectR allows you to target a portion of your book where you can maximize the results and effectiveness of budget resources.

The process for scoring a book using PreInspectR is simple. All that is required is five specific property characteristics from each policy. The scores produced for each property will indicate the likelihood of condition hazards and/or ITV concerns. This allows you to focus on those properties with the highest scores, which in turn will have the highest actionable rate. Using this approach, PreInspectR allows you to target a portion of your book where you can maximize the results and effectiveness of budget resources.

Millennium is pleased to offer this powerful tool as part of our included service, at no fee to our exclusive clients.

Whether it’s inspection optimization models, MAPS advanced inspection workflow technology, a quality support structure, surveys or data analytics, Millennium Information Services has everything your company needs to truly understand your book of business.

Why are physical inspections vital to estimating roof life?

Through our work over the last 25 years, Millennium has developed an extensive inspection database with over 12 million property records, which we regularly analyze to identify trends in specific regions, states and local areas for our clients. One area of particular concern to our clients is roofs. You may be interested to know that we find roof issues on 16.9% of the properties we inspect nationwide.

Through our work over the last 25 years, Millennium has developed an extensive inspection database with over 12 million property records, which we regularly analyze to identify trends in specific regions, states and local areas for our clients. One area of particular concern to our clients is roofs. You may be interested to know that we find roof issues on 16.9% of the properties we inspect nationwide.

At a regional level, the South has the highest incidence of roof conditions at 22.3%, followed by the Northeast 17.9%, Midwest 15.0% and West 12.3%. Millennium provides our clients with data analyses on numerous other hazard conditions including ITV and TLA variances, tree hazards, dangerous dog breeds, unfenced pools and trampolines, uneven sidewalks and driveways, and steps and porches without railings, to name just a few.

In addition to analytical data, Millennium Information Services provides insurance carriers with a crucial element in the underwriting process for commercial, farm and residential properties: a physical inspection report. Our experienced inspectors uncover vital information about an insured premises — information that’s often invisible to the untrained eye and undetectable through aerial imagery, which, in addition to frequently being outdated and incomplete, lacks sufficient visibility of the most common hazards and adverse conditions.

Quality information is essential to successful underwriting. Profitable decisions depend on your ability to get the clearest, most detailed view of both individual properties, broader, regional issues and your complete book of business.

Millennium inspection reports provide detailed documentation on all conditions, risks and hazards observed at the property that may contribute to future loss and claim expenditures, along with a wide array of photographs of the exterior, interior and surrounding premises to convey a true picture of exposure in a property’s current condition. The level of detail we provide enables insurance professionals to make more intelligent underwriting decisions based on comprehensive, up-to-date and accurate property data.

Through our MAPS inspection workflow platform, Millennium gives our clients the ability to mine your own inspection data and conduct analysis on all of the property attributes and characteristics captured in the inspection report. Which hazard conditions are prevalent in your book of business and where are they found? Which agents are driving these quality-of-business issues? Millennium provides you invaluable data and tools to proactively manage your property business, reduce losses and achieve your growth and profitability objectives.

The bottom line is, when it comes to risk assessment and underwriting, it pays to inspect the uninspected.